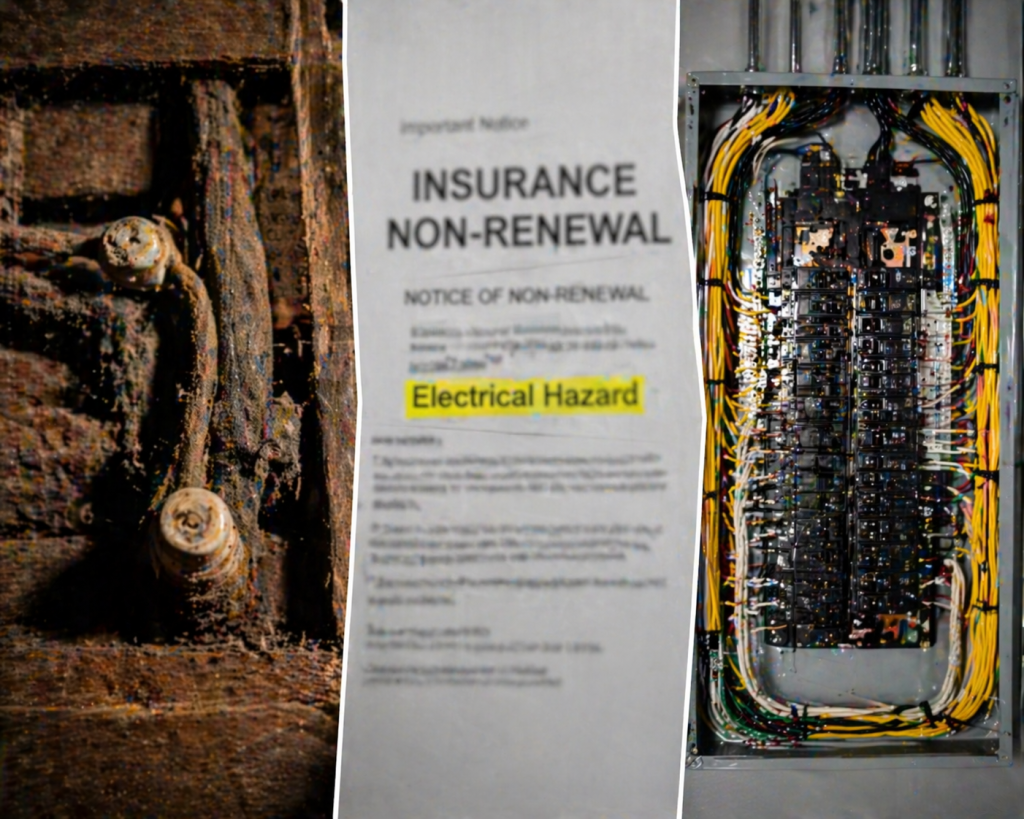

You get a letter from your insurance company. Maybe it is a non-renewal notice. Maybe it is a flat-out cancellation with a 30-day deadline. Maybe you are trying to bind a new policy on a brownstone you just bought and the underwriter calls it off at the last minute. The reason, every time, is the same four words: knob and tube wiring.

This is one of the most common insurance problems NYC brownstone and pre-war homeowners face, and also one of the most solvable if you know exactly what the carrier is looking for and how to present it. Here is the full playbook: why carriers cancel, what your actual options are, and the documentation that quietly gets you re-insured (often within days, not months).

Why Insurance Carriers Are So Strict About Knob-and-Tube

Carriers treat knob-and-tube wiring differently than they treat other old wiring because the failure modes are specifically the ones that trigger expensive claims: electrical fires, smoke damage, total loss. The wiring itself ceramic knobs supporting single-insulated copper conductors was perfectly safe when it was installed in the 1890s to 1940s. What carriers know, and what the data backs up, is that a century of degradation changes that math.

The Three Things Underwriters Are Actually Worried About

- Insulation breakdown. Original cloth-and-rubber insulation becomes brittle over decades, cracks, and exposes live copper inside wall cavities where nobody will find it until something goes wrong.

- Load incompatibility. Circuits designed for a few light bulbs and a radio now run air conditioners, microwaves, space heaters, and laptops. Overload risk is real and measurable.

- Improper modifications. Most K&T failures insurers pay on are not the original wiring failing on its own they are DIY or unlicensed splices tying modern cable into the old system inside ceilings and walls. Every splice is a potential fire initiation point.

Those three concerns are why a carrier’s underwriter, seeing ‘knob and tube active’ on an inspection report, starts pulling numbers from the actuarial table that make your policy unprofitable. Cancellation or non-renewal follows.

How the Cancellation Actually Happens

Most NYC homeowners do not wake up to a cancellation out of nowhere. It usually starts one of three ways:

1. The Home Purchase Inspection

You buy a brownstone. The home inspector notes ‘active knob-and-tube wiring observed in basement ceiling’ in the report. The insurance carrier the buyer binds with during closing pulls the inspection, sees K&T, and either declines to issue, issues with exclusions for electrical fires, or issues short-term with a condition to remediate within 60–90 days.

2. Four-Point or Annual Inspection

Some carriers require periodic electrical inspections on homes over 50 years old. A licensed electrician submits a report. K&T shows up. The carrier sends a non-renewal notice 60 days before the policy anniversary.

3. A Claim Triggered a Review

You filed a claim could be anything, water damage, a break-in, a kitchen fire and the carrier sent an adjuster. The adjuster pulled the panel, followed the wires, and noted active K&T. Even after paying the unrelated claim, they notified you that the policy will not renew.

Our separate guide on whether homeowners insurance covers faulty wiring covers what does and doesn’t get paid on claims worth reading if you’re in the middle of a claims situation.

Your Four Real Options

When the cancellation letter arrives, most homeowners panic and start calling other carriers. That works sometimes, but there is a smarter sequence. Here are the four paths, in order of how most NYC owners actually end up solving it:

Option 1: Full Rewire and Re-Certify

The cleanest and most durable option. You hire a licensed electrician to remove all active K&T circuits, replace them with modern NM-B or armored cable, upgrade the panel if needed, and provide a signed certification that no K&T remains active in the home. Carriers accept this immediately. Budget is the main constraint we cover NYC rewire costs in detail, and the technique for rewiring without tearing down drywall is worth reading if you want to avoid a full renovation.

Option 2: Partial Rewire + Abandonment Certification

Many NYC homes have a mix: K&T in some walls or on a single floor, modern wiring elsewhere. Rewiring everything is expensive and disruptive. What often works with carriers is a partial scope: remove and replace the accessible K&T, disconnect and abandon in place the inaccessible runs (with documentation), and provide a certification that ‘no active knob-and-tube wiring remains.’ This is typically the sweet spot for brownstones where tearing out ornate plaster would be cost-prohibitive.

The key document is the electrician’s abandonment letter, signed and dated, stating specifically which circuits were removed, which were abandoned, and confirming no energized K&T remains in service.

Option 3: Specialty or High-Risk Insurer

Some carriers specifically underwrite older homes with K&T as long as specific conditions are met usually a passing electrical safety inspection, proof of no prior electrical claims, updated panel, and a smoke alarm monitoring system. Premiums run 30–80% higher than a standard policy, but the coverage is real. This is often the right move if rewiring is financially impossible in the short term or if you plan to sell within 2–3 years.

Option 4: Excess & Surplus Lines

If standard and specialty carriers both decline, E&S carriers (Lloyd’s of London syndicates, regional E&S markets) will write policies on almost anything at a price. Expect premiums 2–4x standard, higher deductibles ($5,000–$10,000 common), and often a fire-cause-of-loss exclusion or sub-limit. Use as a bridge, not a long-term solution.

The Documentation Package That Actually Works

Whether you go with Option 1, 2, or 3, carriers ask for the same underlying paperwork. Having all of it ready before you approach the underwriter reduces back-and-forth from weeks to days:

- Licensed electrician’s signed certification stating no active K&T remains (Option 1 or 2) or detailing exactly what K&T remains and what condition it is in (Option 3).

- Scope-of-work summary: which circuits were addressed, dates of work, materials used, panel status.

- DOB electrical filing receipt if the work required a permit (most rewiring work over one circuit does).

- Licensed electrical inspection agency (LEIA) certificate. This is the third-party sign-off required on all NYC electrical work, and carriers give it significant weight.

- Photographs — panel interior (cover off, taken by the electrician), a sampling of junction boxes, any visible modern cable runs.

- Panel upgrade documentation if the panel was replaced as part of the work.

- Smoke and CO detector installation certificate (many carriers require interconnected alarms on all levels as a condition).

A proper electrical safety inspection by a licensed NYC electrician produces most of this package as a natural output. If the cancellation letter is already in your hand, the inspection is step one.

Timing: How Long This Takes

The clock matters. Most cancellation notices give 30 days; non-renewals typically give 60. Here is what a realistic timeline looks like:

| Path | Work Time | Total to New Policy |

| Full rewire (small 2-story brownstone) | 2–4 weeks | 4–6 weeks |

| Partial rewire + abandonment | 1–2 weeks | 2–3 weeks |

| Specialty carrier (existing K&T, documented) | 3–7 days | 1–2 weeks |

| E&S bridge policy | 2–5 days | 1 week |

| Inspection + documentation only (no rewire) | 1 week | 2 weeks |

If your cancellation deadline is inside two weeks and rewiring is not possible in that window, the right move is usually an E&S bridge policy first, then the full remediation, then re-binding with a standard carrier at the next renewal.

NYC-Specific Complications

Brownstones and Landmarked Buildings

If your building is in a historic district or has landmark status, you cannot just open walls freely. Landmarks Preservation Commission (LPC) approval may be required for any exterior work, and board approval (if co-op) for interior. Our Manhattan electrician page covers the neighborhood-specific challenges the same ones that make insurance carriers extra cautious in these buildings.

Co-ops and Condos

If you are in a co-op or condo and the K&T is in common areas (hallways, risers, shared walls), you cannot unilaterally rewire. The board has to approve and often has to pay. This is one of the trickiest situations in NYC insurance — your individual policy may be cancellable over wiring you legally cannot touch. The solution is usually a specialty carrier plus a letter from the board documenting the building’s remediation plan.

Shared Walls and Tenement Conversions

In tenement-conversion buildings, the K&T may snake between apartments through shared wall cavities. Carriers hate this because a fire in a neighbor’s unit can spread via the wiring. The fix is building-wide, not unit-level.

Aluminum Wiring in the Same Home

Some NYC homes built 1965–1975 have a combination of K&T remnants in the older parts and aluminum wiring in the mid-century additions. Both are insurance red flags. Our guide to aluminum wiring in older NYC homes covers the remediation path for that specific combination.

What To Do This Week

If you just received a cancellation or non-renewal notice, here is the concrete sequence:

- Day 1 — Read the letter carefully. Identify the exact deadline and the exact reason. ‘Knob-and-tube wiring’ is different from ‘substandard electrical system’ in how carriers will process the re-binding.

- Day 2–3 — Call a licensed NYC electrician to schedule a safety inspection. Be clear on the phone that you have an insurance deadline; most electricians prioritize these jobs.

- Day 4–7 — Get the inspection. Ask for a written findings report and, if possible, a scope-of-work quote for full rewire and for partial rewire + abandonment.

- Day 8–10 — Contact your insurance broker with the inspection findings. Ask which carriers will bind with which scope of remediation. Pick the path that fits your budget and timeline.

- Day 11–14 — Schedule the work. Make sure the electrician will provide the certification letter, LEIA certificate, and DOB filing documentation.

- Before the deadline Submit documentation to the carrier (or to the new carrier) and request the policy.

A&B Electric Wiring has done this rewire-for-insurance-deadline work for dozens of NYC homeowners. Get in touch and mention the insurance deadline on the first call we schedule these ahead of routine work whenever possible.

Frequently Asked Questions

My inspection just found knob-and-tube. Should I tell my insurance company?

Most policies have a material change clause that technically requires disclosure. In practice, if your existing policy is in force and no claim is pending, the smarter move is to remediate first and then disclose the abandonment as an improvement. Talk to your broker about your specific carrier’s rules before deciding.

Can I just rewire the visible circuits and leave the ones in the walls?

Leaving K&T active in the walls is the exact situation carriers are trying to avoid. The valid version of this is partial rewire with full abandonment of inaccessible runs the difference is that abandoned runs are physically disconnected at both ends, not just ignored.

Is ‘grandfathered’ knob-and-tube still insurable?

Some carriers say yes, most say no. Being code-grandfathered means the city won’t force you to remove it. It does not mean insurers will cover it. These are separate questions.

Will rewiring increase my home’s value enough to pay for itself?

In NYC, yes most brownstone appraisers and buyers’ agents treat documented recent rewire as a significant positive. It also removes the K&T disclosure that would otherwise reduce offers at sale. Our K&T in NYC brownstones blog covers the resale math in more detail.

Can the electrician pull permits retroactively if I already had work done?

Not really. DOB filings have to be submitted before the work or concurrently. Unpermitted electrical work creates its own insurance and resale problems. If you inherited unpermitted work from a prior owner, a licensed electrician can do a remediation inspection and file for the current condition, which is as close to retroactive as the system allows.

Bottom Line

A knob-and-tube-related insurance cancellation feels like a crisis when the letter arrives, and it is but it is also one of the most routine problems NYC licensed electricians solve. The path is known, the documentation is standardized, and the carriers that write these policies have a predictable checklist.

The two things that waste the most time: waiting too long after the cancellation letter arrives, and trying to solve it with brokers before you have an inspection report in hand. Start with the inspection, then let the inspection dictate the scope, the scope dictate the budget, and the budget dictate the carrier path.

For a fast-turnaround electrical safety inspection and rewire quote in NYC, A&B Electric Wiring serves Manhattan, Brooklyn, Queens, the Bronx, and Staten Island. Reach out for same-week inspection appointments, or see our full range of residential electrical services including panel upgrades that often pair with rewiring work for insurance documentation.